Retro Plans for Workers Compensation

Companies who manage their workers comp risk and claims can save big with Retro Plans.

What is Retro Plan for Workers Compensation?

- Secure

- Fast

- Easy

Retrospective Rating & Workers' Comp

What is a Retro Policy?

Workers compensation Retrospective Rating Plans are insurance policies with a built in mechanism to allow employers to share in the financial risk and reward with regard to their insurance coverage. Retro plans are typically designed for companies that pay $250,000 or more for a standard workers comp policy.

In a nutshell, Retro Plans can shave up to 75% off traditional coverage or they can significantly increase the cost of coverage depending on the actual losses during the policy period. Retro plans can be beneficial for companies with low experience mod's (credit modifiers), but they can also benefit companies with high modifiers (debit modifier) if the business can reduce claim frequency and loss severity during future policy periods.

Many insurance experts believe the workers compensation insurance market cycles between a hard insurance market and a soft insurance market every 3 - 5 years. Employers with larger insurance premiums often bear the burden of greater costs during an hard market. Retro Plans can be a good tool to control insurance costs for smart and stable employers with premiums over $250,000 per year.

Example of a Retro Workers Comp Program

| Standard Annual Premium | $500,000 |

| Maximum Premium Factor | x 1.12% |

| Maximum Annual Premium Cap | $560,000 |

| Standard Premium | 500,000 |

| Basic Premium Ratio | x .0415% |

| Basic Premium | $207,500 |

| Losses During Year (paid claims) | $50,000 |

| Loss Conversion Factor | x 1.12% |

| Converted Losses | $56,000 |

| Basic Premium | $207,500 |

| Converted Losses | $56,000 |

| Pre-Tax Cost of Retro Coverage | $263,500 |

| Tax Multiplier | x 1.070 |

| Retro Premium Amount | $281,945 |

| Normal Expected Non-Retro Premium | $500,000 |

| Estimated Premium Return (savings) | $218,055 |

| *Ratings vary between factors for Retro Plan insurance. Final calculation of premium and premium adjustments often occur up to 3 years after the policy if claims are still open or loss development is expected. Contact Workers Compensation Shop.com for underwriting information or questions about Retro Plan quotes. | |

Understanding Retro Insurance Coverage

Retrospective Rating has the potential for risk and reward. Many entrepreneurs already understand the concept of retro plan coverage because they are used to taking risks to reap financial reward.

- Maximum premium - standard premium x max factor

- Basic premium - standard premium x basic factor

- Minimum premium - basic premium x tax multiplier

- Converted losses - incurred losses x loss conversion factor

- Retro premium - basic premium + converted losses x tax multiplier

- Plan premium - basic premium x loss ratio x loss conversion x tax multiplier + min premium

- Percentage of Losses to reach max premium - (max prem - min prem) / tax multiplier / loss conversion / normal premium

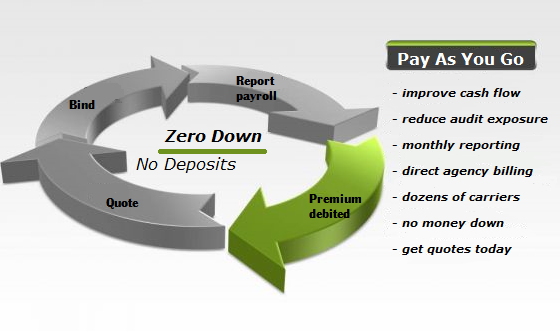

Billing and Coverage Options

Retrospective Rating Formulas

A retrospective rating formula is determined by the insurance company after reviewing prior loss history, class codes, and policy history. The formula is predicated off of the Basic Premium, or no loss premium. The Basic Premium is the starting point for the rating formula and is the minimum cost of coverage based on zero claims during the period. The formula is then applied to the policy based on the actual and reserved cost of claims as the policy moves forward.

Front Loaded Retro Plans

Workers Compensation Shop.com offer front loaded Retro Plans that allow employers to report and pay premium each month based on their actual payroll. The program continuously monitors anticipated and actual losses and adjusts the net billing rates based on the exposure and losses. Our Retro Plan is available to companies with a standard premium of $250,000 and up. Not all companies will qualify.

Retrospective Rating Plans

Retrospective means to review the past or to apply to past events. Retro Plans are designed to apply workers' compensation premium retrospectively to the past based on actual incurred losses and claim costs during the policy period.

Retro plans place the insurance company into more of an administrative and policy management role and reduces their risk by shifting a percentage of potential claim costs to the employer. The insurance company is able to better predict their overhead costs and potential claims costs which enables them to lower minimum premium for coverage.

A Retrospective plan is not an actual workers compensation policy; its an endorsement to a policy that includes the rating formulas used to calculate premiums. The two most common types of Retro Plans include a) Incurred Loss Retro Plans and b) Paid Loss Retro Plans.

PRICE CHECK

Get a free insurance comparison today and see if your business qualifies for lower rates.

How Does Workers' Compensation

Work?

- What is Workers Compensation?

- The Basics of Workers Comp

- Workers Compensation Q and A?

- Insurance Laws for Work Comp

- Managing Policy Claims

- Getting Work Comp Benefits

- NCCI Classification Codes

- Experience Modifiers and Ratings

- State Fund Insurance

- Handling Workers Comp Audits

- Understanding an Employer Liability Policy

- Excluding Owners and Officers

- Multi-State Coverage

Our Best Selling Workers' Comp

Programs

We Manage Large Workers' Comp Plans

California DBA: I-Shop Online Insurance Agency.