Direct Bill Workers Compensation

Our direct workers' comp billing plans are good for small business premiums and consistent payrolls.

Pick a workers comp plan that works for your business

- Secure

- Fast

- Easy

Direct Bill Workers Comp Installments

What is a Direct Bill Policy?

Workers Compensation Shop.com writes direct bill workmans compensation insurance for all types of employers. Our direct bill payment plans are the standard billing option for retail workers compensation. Most employers are used to purchasing this type of policy because it is the industry norm.

Direct Bill insurance refers to the way a policy is billed. It indicates that the policy holder will be billed directly by the insurance company once a workers comp policy is bound (sold) and the deposit premium is collected by the agent or billed by the insurance company. Direct bill workers' comp is the most traditional way in which most business owners purchase work comp policies.

Traditionally, insurance companies have required a deposit of 15% to 25% down in order to start, or bind, a policy. Carriers will then bill the remaining premium balance over 3 to 9 installments. While this is a good billing option for many small businesses with consistent payroll, it can create the following issues for some employers:

- It can require a more significant amount of cash in order to start (bind) a policy

- Billing is usually based on the first 3 to 9 months which can create cash flow issues since income is earned throughout the entire year

Keep in mind that traditional Direct Bill work comp is based on estimated payroll and subject to an annual year-end audit. If your actual payroll ends up higher than your estimated payroll, you will more than likely owe additional premium as a result of the audit.

Example: 6 Installments; $5,000 Insurance Policy:

| Annual Premium: | $5,000.00 |

| Carrier Expense Constant: | $200.00 |

| State Surcharge/Tax: | $30.00 |

| 25% Deposit: | $1,307.50 |

| Remaining 6 Installments: | $653.75 |

Typical Payment and Billing Options:

- Installment checks by mail

- Payments over the phone by bank or credit cards

- Online payments

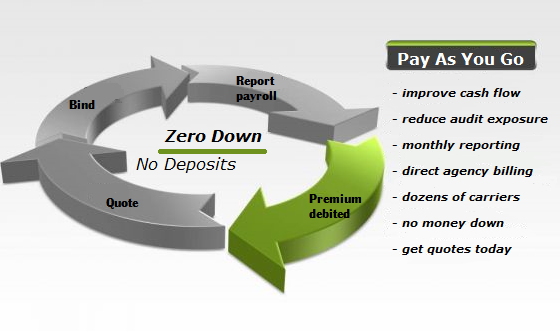

- Direct Pay As You Go options

- Agency bill Pay As You Go

- Monthly Self Reporting

Direct Bill workers compensation billing is a perfect solution for small businesses who have a low premium (typically under $5,000), predictable payroll, and extra operating capital. Employers who have payroll that tend to fluctuate or larger premiums may be better served by getting quotes for self monthly reporting work comp plans or Pay As You Go workers comp programs.

Billing and Coverage Options

What is an Expense Constant?

An Expense constant is a flat dollar amount added to the Pure Premium on every workers comp quote or policy. The expense constant represents a flat administrative charge kept by the insurance companies for overhead costs. It serves the purpose of covering the cost of issuing and servicing an insurance policy regardless of any claims or losses.

State 2nd Injury Funds and Workers Comp

State fund surcharges are designed to protect employers from the higher cost of insurance that can occur when an injury combines with a prior disability to result in substantially increased medical or disability costs than the accident alone would have produced. These funds are designed to ensure that an employer is not made to suffer a greater monetary loss or increased insurance costs because they hire or retain an employee who has a disability. 2nd Injury Funds also help ensure the payment of workers' compensation benefits to injured employees who worked for employers who failed to obtain coverage for employees.

Why Billing Matters?

For some industries such as business offices and small retail stores, workers compensation is typically not a tremendous expense compared to other lines of coverage. Additionally, similar types of businesses have predictable labor cost which makes it easy to accurately guess the overall annual premium for workers' compensation coverage.

There are other industries, such as contractors and restaurants, where workers' comp is the single largest insurance expense for the business. Many of these same businesses struggle with fluctuating payrolls which leads to potential audit issues at the end of the policy period.

It might make sense for some employers to pay their premium in full or make payments over a few installments for part of the year. However, employers with significant payroll, higher workers' comp rates per class code, or unpredictable payroll, other billing plans might prove to be more beneficial to improve cash flow or reduce audit exposures.

PRICE CHECK

Get a free insurance comparison today and see if your business qualifies for lower rates.

How Does Workers' Compensation Work?

- What is Workers' Compensation?

- How Much is Workers Comp?

- Experience Modifiers & EMR Ratings

- Workers' Comp Class Codes

- 1099 vs W-2 Employee

- Workers Compensation Basics

- Employers Liability Insurance

- Workers' Compensation FAQ's

- Multi-State Insurance

- Workers' Compensation Laws

- State Insurance Fund

- Workers' Comp Claims

- Workers Compensation Benefits

- Managing Workers Comp Audits

- Workers' Comp Exemptions

- Ghost Policy

Our Best Selling Workers' Comp Programs

WHY SHOP WORKERS COMP WITH US?

MORE THAN 35 CARRIERS TO QUOTE

We work with over 35 workers comp insurance companies across the U.S to shop your insurance coverage for the best price.

LOWER MONTHLY PAYMENT PLANS

With dozens of Pay As You Go and easy installment plans to choose from, you get more flexible options for your business.

EXCLUSIVE WORK COMP PROGRAMS

We've developed Target Programs with our insurance companies to help find you the right insurance product with lower rates.

California DBA: I-Shop Online Insurance Agency.