How Much is Workers' Comp Insurance?

The cost of workers compensation is regulated at the state level. Rates will also vary by assigned class codes, estimated payroll, claims, agent and insurance company.

Understanding the cost of coverage.

Workers' Comp Questions? Call 888-611-7467 for a Workers' Compensation Specialist

The Cost of Workers Comp is Regulated by Each State

Workers comp pricing is based on several factors. The lowest and the highest rates a workers comp insurance company can charge is filed set and reviewed by each states' insurance regulators. Insurance companies must file their own rates for approval each year. These rates must be within the minimum and maximum range permitted.

To prevent insurance companies from under-cutting rates and becoming insolvent, insurance company rates are regulated by a factor known as the Loss Cost Multiplier (LCM). The LCM is a factor that measures each insurance companies' loss ratios to make sure they have enough money to fund insurance claims. After the rates are filed for approval, they are either approved or rejected. This is how the rate process begins with each workers compensation insurance company.

How is Workers' Comp Premium Calculated?

Once an insurance company has the authority to sell workers compensation insurance within a state, they determine which class codes they want to target and how aggressive they want to be on pricing each work comp policy. Insurance companies utilize the following in order to determine the estimated cost of workers comp:

Covered States

Business Industry

Annual Payroll

Here is an example using two class codes with different estimated payroll for each class code:

| Carrier Rate Per $100 | Estimated Payroll | Divide by 100 |

|---|---|---|

| $0.28 base manual rate | $25,000 (25000 divided by 100) | 250 |

| $1.75 base manual rate | $100,000 (100000 divided by 100) | 1000 |

In order to calculate the cost of workers comp you will need to multiply each class code rate with its divided payroll amount.

| Class Code | Workers Comp Calculation | Estimated Premium |

|---|---|---|

| 8810 Clerical | $0.28 X 250 | $70.00 |

| 8835 Home Health Care | $1.75 X 1000 | $1,750.00 |

Business Characteristics

Claims History

Work Comp Insurance- click or call!

m-f 8am-5pm CST 888-611-7467

Credits and Debits Adjust the Cost of Workers Comp

Insurance companies decide what industries and class codes they want to cover. If they don't think they can be profitable in a higher risk business like roofing or trucking, they can choose not to offer a quote. If they are willing to quote they can decide how aggressive they want to be on pricing. Its the underwriters job to make that decision and the agents job to advocate for the lowest cost.

In most states, the insurance company can apply credits or debits to their pricing to reduce or increase the premium. Credits or debits are applied based on the underwriters review of the business and can often be as high as 25% credit or 25% debit. That's a 50% swing in price. Most business owners don't know that most big insurance carriers own multiple subsidiary workers' compensation companies under their portfolio. This is referred to as Writing Papers. When insurance companies file multiple sets of rates with the state regulatory authority, it gives them more flexibility to compete with other insurance providers by manipulating the writing paper to control the overall premium cost.

Class codes considered lower-risk have lower rates with multiple insurance companies willing to quote. Higher-risk class codes have higher rates and fewer insurance companies willing to offer a work comp quote. Insurance Companies decide which industries they want to target, industries they are cautious but willing to quote and industries they will not quote under any circumstance.

Premium Discounts are Applied to Bigger Policies

It seems appropriate that the bigger a business is, the more it will pay for coverage. A business with more employees will have a higher payroll. Since premiums are based on a factor of (payroll divided by 100) x (class code rate), the result will be a higher overall cost. However, once worker's comp premium hits a certain dollar threshold (usually $5,000), most states require insurance companies to begin applying additional discounts on the policy. This volume discount is given because the administrative overhead for the carrier should decrease as the number of employees increases.

Risk Affects How Much a Business Pays for Workers' Compensation

Class codes considered lower-risk will have lower rates with multiple insurance companies willing to offer quote. Higher-risk class codes will have higher rates and fewer insurance companies willing to offer a work comp quote. Insurance Companies decide which industries they want to target, industries they are cautious but willing to quote and industries they will not quote under any circumstance.

Higher-risk businesses, such as construction and tree service, experience more claims that cost more on average to close. They also represent the majority of death claims. NCCI collects and shares the statistical claims data for each state.

Loss Runs and Claims Reporting

One underwriting requirement that greatly affects pricing is any applicable workers' compensation claims history for the past 3-4 years. This history is also known as a Loss Run Report. Insurance companies are required to provide any business they have insured with this report, as requested by the insured. The Loss Run Report shows the year/s of coverage with that insurance company and the details of any claims the business suffered. When a businesses can show they have had little to no claims, a good agent will work to negotiate lower rates with underwriters. They will also increase rates or decline to quote coverage if the claims incurred are too frequent or costly.

How to Control the Cost of Workers Comp?

Implementing, enforcing and documenting good business practices have a big impact on the underwriter’s willingness to write tough classes and offer credits on a policy. Experienced agents that have good connections with their underwriters will ask questions about what precautions a business takes to reduce or eliminate the possibility of claims. Experienced agents will highlight to the underwriter the steps a business takes to prevent claims when presenting your business info for quoting. Good business practices include good hiring practices, safety training and documentation of that training, a return-to-work program, checking motor vehicle reports for employees that drive while working, physicals where applicable, offering health insurance to employees and an overall attitude towards safety in the workplace.

Make payments on-time and complete audits promptly. This can be a big factor when negotiating annual renewals. If payments are made on-time and the audit is completed timely, Insurance companies and their underwriters will value the business more. Prior cancellation notices and reinstatements throughout a policy period may be a cause of increased renewal offers.

How Relationships Affect

the Cost of Coverage?

the Cost of Coverage?

An agents relationship with an underwriter has a big impact on pricing. Insurance companies want to maximize profits. They are looking for good insurance customers with minimal losses. If an agent's book of business is not profitable to the insurance company, and that agent continues to insure business that suffers costly claims, the insurance companies becomes less likely to quote competitively for the agent, even if it’s a target industry.

Underwriters appreciate agencies they trust, such as Workers Compensation Shop. They are willing to take more risk with these partners. Insurance companies are much more likely to trust agents with healthy, profitable books of business that include correct class codes and accurate audits. Agents will often receive better pricing and higher approval odds for a piece of business they are on-the-fence with.

Smart agencies know what their insurance companies and underwriters want to quote and how they want the business information laid out, making it easier for them to make an affirmative decision.

Underwriters have production goals to meet, but they must meet those goals while maintaining a positive loss ratio. If an agent's book of business is not profitable for the insurance company, underwriters become less likely to offer the most competitive quotes. This occurs because if the agent continues to insure businesses that have costly claims, both the agent and the carrier will become unprofitable. This may occur even if the business is in a target industry for the carrier. Underwriters don't make exceptions or offer credits to poorly performing agencies. Some underwriters may try to reverse the loss ratio for that book of business. They do that by declining tougher risks, increasing rates and eliminating credits and discounts for new business quotes.

Compare Work Comp Rates

Save 30% on work comp for select businesses

- What is Workers Compensation?

- The Basics of Workers Comp

- Workers Compensation Q and A?

- Insurance Laws for Work Comp

- Managing Policy Claims

- Getting Work Comp Benefits

- NCCI Classification Codes

- Experience Modifiers and Ratings

- State Fund Insurance

- Handling Workers Comp Audits

- Understanding an Employer Liability Policy

- Excluding Owners and Officers

- Multi-State Coverage

Policy Credit

A policy credit is a subjective adjustment made by underwriters to reduce or increase how much a workers comp policy with cost. Credits need to be requested by the agent and justified by the underwriter.

Premium Discount

A volume discount applied to premium above 5,000 to account for reduced administrative overhead for the insurance company as premium grows larger. The discount is graduated based on the estimated and actual premium paid.

Base Manual Rate

A base manual rate, or manual rate is the rate filed with the state insurance regulators by each insurance company. It is the starting rate before any credits or debits are applied to a policy or quote.

Loss Runs

A loss run report is a insurance company report outlining the details of any claims for each policy period where they provided insurance coverage. This included date, description of claim, reserved expenses and incurred expenses.

LCM- Loss Cost Multiplier

Insurance companies file their LCM with each state. This factor represents the insurance companies adjustment to the actual expected claims expenses for each class code. The LCM represents the states expected expenses plus the insurance companies' own experience with expenses.

Help With Work Comp Pricing?

Our expert staff help large and small business owners with the administration of workers comp. Let us show you how much we can save you on your next quote.

We help with employee classification, owner exemptions, payroll rules and more. See if one of our Target programs or Pay As You Go plans are right for your business. You will be glad you did.

Get workers compensation quotes from trusted experts who help shop and manage your policy better.

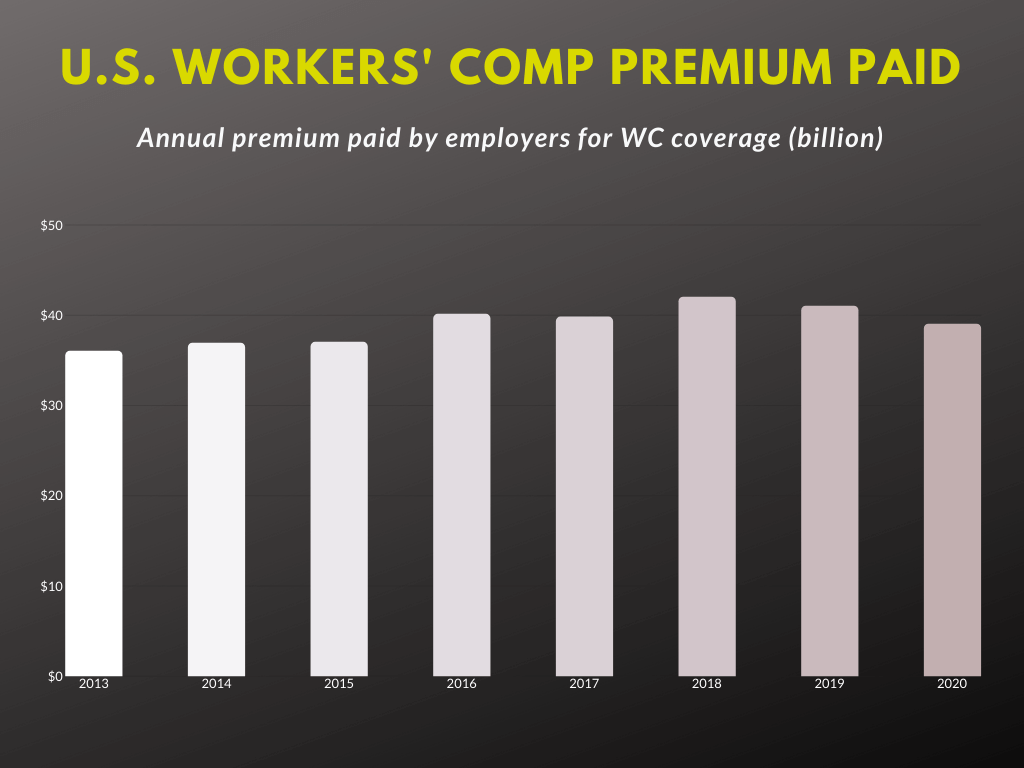

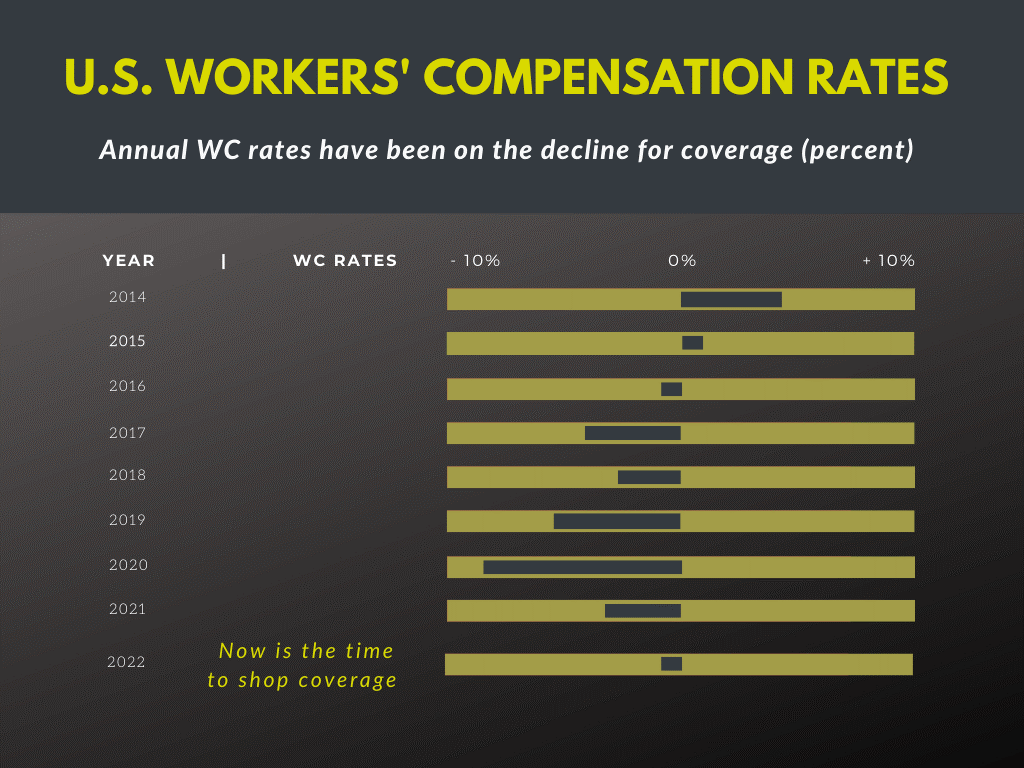

U.S. Annual Cost of Workers' Comp & Average Rate Changes

Ready to Start Your Quote?

Don't settle for cookie-cutter rates

- Secure

- Fast

- Easy

California DBA: I-Shop Online Insurance Agency.