Workers' Compensation Rates

Rates for workers' comp are generally determined by a number of underwriting factors and will vary by state, insurance company, payroll and class codes.

Workers' comp rates are different in each state.

Understanding Workers' Compensation Rates (2020)

There are a number of factors that go into workers' comp rate-making. Most states require each insurance company to file their manual rates for approval each year. Manual rates are only a beginning point for the quote process. Rates can be manipulated in several ways to arrive at the final premium rate used to determine the cost for coverage.

Several technical factors such as Emod, size of premium, and prior claims drive workers' comp rating. There are also other subjective factors that affect rates such as management experience and and safety considerations. An agents access to, and relationship with, various private insurance companies also influence the overall cost of a policy.

Workers' compensation rates are both an art and a science. In fact, rates and class code eligibility are often negotiable between agents and underwriters. Some agencies have better relationships and more profitable policies with insurance companies.

Looking for information on how rates are calculated?

How is Workers' Comp Premium Calculated?

Cost of Living & Losses Affect State Rates

State workers' compensation rates are designed to reflect the cost of claims and losses for scope of job, or class code. Class codes with greater loss frequency and/or severity will cost more based on the statistical data of any given state. However, the loss data for similar class codes can be significantly different by state. These calculations consider factors such as the number of claims, cost of medical services, and the cost of replacing lost wages in the state. Since states will have varying results in terms of frequency and severity, rates will vary to reflect and account for the experience of each state.

As an example, lets compare Missouri and California. The average wage and the average cost of medical care is much lower in Missouri. The average wage is also lower to reflect the cost of living. Therefore, the overall cost of a claim and replacement of lost wages would be less in Missouri than the costs associated with the same claims in California. Rates will generally be lower in Missouri for most class codes. Anomalies can exist when certain states have a disproportionate quantity of certain industries within classes of business. Logging and manufacturing are examples of industries that may be more regional than national.

The Average Cost of Workers' Comp Insurance?

The average rate for an office employee doing clerical work is less that $0.35 per $100 in payroll wages. The average cost for a roofer is over $19.00 per $100 payroll. It's more useful to think about work comp rates in context of class codes. The only way to know if you are getting a good rate is to understand the low and the high range for the class codes used for your business coverage.

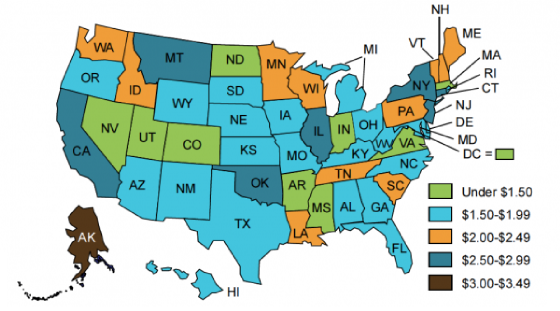

The map below represents the average combined cost per $100 for all class codes in each state. Notice that states with the highest rates tend to either be states with a high cost of living and states where access to medical care could drive up the cost of claims. State laws can also affect rates because they affect medical and disability payment rules that will impact claim costs.

Workers' Compensation Insurance

Average Cost by State

Who Sets Workers' Compensation Rates?

Monopolistic states and a few other states such as Florida, and Wisconsin set the base manual rates that all insurance companies must use for each class code. Most other states allow private insurance companies to file their manual rates within the guidelines set by the state. New Jersey also sets workers' comp rates, but insurance companies are permitted to offer a limited range of policy credits and debits. New York allows carriers to set their own rates, but does not allow additional policy credits and debits.

Many larger insurance companies own additional subsidiary insurance companies so they can file multiple sets of rates for the same states. Within the insurance industry, this practice is known having separate writing papers for insurance pricing. This strategy enables the insurance company to file competitive rates as well as less competitive rates depending on the desirability of a particular business and class codes associated with the risk.

By utilizing multiple writing papers, insurance companies can file and use multiple rating tiers to price coverage within most states. Underwriters from the insurance company can then determine which writing paper to use based on loss history, management experience, premium size, alternate quotes and other underwriting factors. Knowledgeable insurance agents can often influence which set of rates (writing papers) gets used on the quote better understanding and marketing your business.

What Determines Workers Compensation Rates?

- Payroll and Premium Discounts

- Experience Modification Factors

- Scheduled Credits and Debits

- State Credits

How Payroll Affects Workers Comp Rates?

The basis of determining premium for a workers compensation policy is payroll. The class code is assigned a rate that is based on each $100.00 of payroll. A work comp rate of 2.5 equates to $2.50 per every hundred dollars of payroll in that class code. Workers' comp payroll is calculated by dividing the gross payroll by 100 and then multiplying by the rate.

$100,000 divided by 100 equals 1000

$1000 multiplied by 2.50 equals $2,500

Annual premium would be $2,500 for this example

Other credits and debits may need to be applied to the manual rate in order to determine the actual net rate used for the calculations

Most states require insurance carriers to apply a premium discount to premiums that hit a certain dollar amount. This discount will affect the manual rate. It is based on the theory that there are fixed costs associated with servicing a workers' compensation policy. Larger premiums receive these credits because the relative expense of these fixed costs should be lower as premium increases. Most states issue a Premium Discount Table for insurance companies to use when rating insurance. Premium discounts generally run between 4% and 10% depending on the total premium size. They are always subject to an audit and will change if the estimated payroll is higher or lower than the actual premium.

How an EMR Rating Adjusts Workers' Comp Rates?

An Experience Modification Rate (also known as EMR, MOD, or EMOD) can be the single most impactful and controllable factor in determining the workers' compensation costs for a business. An Emod is the numerical representation of how your claims experience compares to other similar businesses within your state. Employers essentially start our with a MOD of 1.00. This means they pay 100% of the rate assigned to the classification code by the insurance carrier with no automatic credit or debit adjustments.

Looking for information on how EMR Rating impact rates?

A Good Experience Modification Rate (EMR) Will Reduce the Cost of Coverage.

Once an employer has had active coverage for 2-3 they become eligible for an experience modification rate. This EMOD is a factor that makes a mandatory adjustment to manual rates. It changes each year and typically coincides with your policy renewal effective date. Insurance companies must apply the EMR Rating to their rates under state laws.

There are two types of Emod's: a Debit Emod and Credit Emod. A Credit Emod is any factor less than 1.00. A Debit Emod is any factor greater than 1.00. The Modification factor is applied to the policy premium in order to reduce or increase the cost of coverage. They are based on the loss history of the business. A Good EMR Rating is anything under 1.00. Great EMR Ratings are anything under .85.

Since they adjust premium, they are actually adjusting the rates a business pays for each class code. For example, Let's assume the manual rate for a class code is $1.00 per hundred, an EMR Rating of .80 would reduce the $1.00 rate to $0.80 cents per $100 of payroll. Conversely, an EMR Rating of 1.20 would increase the rate to $1.20 per $100 of payroll. Emod can also be applied to the overall cost of the policy as well. A .85 Emod would reduce a $2500 premium by 15% ($2,125).

Scheduled Credits and Debits Manipulate Rates

Most states permit insurance companies to apply scheduled credits and debits to workers' compensation coverage in order to adjust an employers' premium up or down. These scheduled credits and debits can be very subjective as they are used at an underwriters discretion. They enable an insurance underwriter to offer manipulate pricing based on unique conditions within a business such as years of experience, safety training, hazardous equipment, work environment, etc.

In some ways, credits and debits undermine the process of filing rates for approved under state laws. Insurance companies can quickly and easily arrive at workers comp cost they think we sell the coverage.

State insurance departments generally require that the insurance companies document the reason for any scheduled credits and debits, but they are commonly used tools for underwriting and adjusting the cost of workers compensation. Generally speaking, states either allow scheduled debits and credits up to 15% or 25% of premium. These adjustments can have a big impact on an employers' overall workers comp rates.

State Credits and Workers' Comp Rates

Many states require insurance companies to offer additional automatic credits to employers who take specific steps aimed at reducing the frequency or severity of workers' comp related injuries and claims. The two most common types of state credits include formal safety programs and drug programs. These credits generally require an employer to create and submit a formal drug policy and/or safety program to the state. A business can received additional premium credits between 3% and 5% of their insurance premium.

State credits vary by state and by their percentage amount. Small business owners often do not know these credits exist as many insurance agents and insurance companies do little to help business owners qualify for these programs.

How to Get Lower

Work Comp

Rates?

Work Comp Rates?

When you consider all the factors used to determine a businesses workers' comp rates, its easy to appreciate how much the final rates can vary between two similar classes of business within the same state. Scheduled credits and debits, EMR ratings, premium discounts, and state credits can double the workers' comp costs of one business while cutting the cost in half for another owner.

Business owners should be focused on preventing and/or managing claims to help protect their Emod. Employers should also be selective in what agents they choose to represent their business. Insurance company underwriters view businesses as potential risk. Good agent help qualify their customers for additional underwriting credits or state credits available to them.

A knowledgeable workers' comp agent understand that the true value-proposition for business owners' is based on their ability to negotiate lower rates with insurance companies. They should also provide additional services to help manage experience modification rates and other possible policy credits. At Workers Compensation Shop.com, we're committed to helping small business achieve the lowest costs on their workers comp coverage.

How do I get started?

- Business details, locations, FEIN or SSN

- Estimated annual payroll and job duties- class codes

- Claims info or loss history- if applicable

- Experience Modification Rate- if applicable

How Does Workers' Compensation Work?

- What is Workers' Compensation?

- How Much is Workers Comp?

- Experience Modifiers & EMR Ratings

- Workers' Comp Class Codes

- 1099 vs W-2 Employee

- Workers Compensation Basics

- Employers Liability Insurance

- Workers' Compensation FAQ's

- Multi-State Insurance

- Workers' Compensation Laws

- State Insurance Fund

- Workers' Comp Claims

- Workers Compensation Benefits

- Managing Workers Comp Audits

- Workers' Comp Exemptions

- Ghost Policy

Final Billing Rates

Business owners sometimes get confused when comparing the cost of workers' compensation from multiple insurance companies. Quotes can only be fairly compared when they utilize the same payroll estimates and class codes. Otherwise. there is no basis for an accurate comparison and the price can be misleading.

Most quotes will only show you the manual rates which do not accurately reflect with actual rates used to calculate the rate per $100 of remuneration (cost of premium). The credits and debits applied to the policy will increase or decrease the manual rates listed on the quote.

In order to determine the real net billing rates for a policy, the total percentage of credits and debits needs to be calculated and applied to the manual rates quoted.

We Compare Rates:

You Get Better Quotes

You Get Better Quotes

Direct Pay As You Go

Easy Pay As You Go workers' comp for business owners who process their own payroll or prefer to report directly to us. No premium requirements, easy underwriting, and fast quotes.

Direct PaygoPayroll Plus Workers' Comp

Outsource your payroll to one of our licensed payroll partners or ask us to work with your current provider.

Payroll and Pay as You GoPay As You Go for Payroll Bureaus

Pay As You Go workers' comp for Payroll Bureaus. Back-office administration and monthly reporting for all active customers.

Back-Office PayGoNational Broker Services

A lot of good insurance agents turn to us for Pay As You Go solutions and better priced coverage. We help other agents solve coverage problems.

Workers' Comp BrokersLets Lower Your Workers' Comp Insurance Cost

Our Quote Process Makes us Your Best Choice for Getting Coverage

- Proprietary comparative rating software

- More coverage options and available markets

- Knowledgeable workers' compensation specialists

- Strong relationships to negotiate the best price

Workers' Comp Rates by State

Our agency software tracks and compares the average workers' comp rates for our insurance companies for select business class codes. We use this data to choose partners that are ready to negotiate the best price for your coverage based on state, class codes, claims and unique business aspects.

If you have questions about your insurance rates or think you might qualify for lower rates, contact one of our Workers' Comp Specialist for a free no-obligation policy review. Talk to an expert at 1-888-611-7467 M-F, 8-5 CST.

California DBA: I-Shop Online Insurance Agency.