What are Workers Compensation Benefits?

Workers' compensation insurance provides financial benefits to employees when they have an injury or an illness caused on the job.

What does workers comp pay for?

Benefits of Workers' Compensation

There are four basic types of workers' comp benefits paid by insurance companies

Workers' compensation benefits are the payments an insurance company makes to the insured's injured employee, or another related party, based on the terms of the insurance policy. Types of payments include:

- Medical benefits

Pays for necessary medical care to treat work-related injuries or illness.

- Income benefits (disability benefits)

Replaces a portion of any wages lost because of work-related injury or illness.

- Death benefits

Pay a portion of lost family income for eligible family members of employees killed on the job.

- Burial benefits

Pays for some of a deceased employee's funeral expenses.

Workers' Compensation Medical Benefits

Medical benefits are are payments made for the medical treatment of a work-related injury or illness. Their is no maximum threshold for medical benefits. Insurance companies will not pay for the treatment of other injuries or illnesses unrelated to the job injury, even if the treatment was provided at the same time as the treatment for a work-related injury. Health care provider should not bill the carrier for treatment related to a work-related injury or illness, but may bill you for treatment of other injuries or illnesses.

All employees have the right to receive necessary medical treatment immediately after the work-related injury or illness. If the business has elected to contract with a certified workers' compensation health care network (network), injured workers may be required to obtain medical treatment through the network

A doctor may only request payment from you or the carrier when the work-related injury or illness has been reviewed by a case manager for dispute resolution, and the injury has been determined to be an injury or illness that is work-related.

It generally beneficial to all parties if injured employees return to work as quickly as possible. Injured employees that continue to work as part of their recovery/treatment plan, in medically appropriate productive work, heal faster, and are more likely to retain their job skills. There is not always a specific end date for reasonable and necessary medical treatment for a work related injury. Getting employees back to work often costs less and helps reduce long-term insurance premiums caused by increased EMR Rating.

Workers' Comp Disability Benefits

Disability benefits are also known as supplemental, income and cash benefits. There are four types of income benefits:

- Temporary income benefits

- Impairment income benefits

- Supplemental income benefits

- Lifetime income benefits

How much does workers comp pay for lost wages?

Injured workers' will generally receive 66 2/3% of their average weekly wage for temporary income or lost wages. However, the amount is capped by the state's average weekly wage. For example, in West Virginia, the average weekly wage is $586. This would be the maximum amount paid to an injured employee out of work due to a disability.

Employees must report any income (other than income benefits they may be receiving) to the Division of Workers' Compensation and the insurance carrier so an adjustment can be made to your income benefit payments. Employees may be fined and/or charged with fraud if they receive temporary income benefits while also receiving wages from an employer without notifying the Division of Insurance and the insurance carrier.

Income benefits are no longer payable following the death of an injured employee receiving income benefits. The injured employee's beneficiaries may be eligible to apply and receive death benefits if the injured employee's death was due to the work-related injury or illness.

How long will workman's comp pay?

Most disability payments are capped between 2-4 years if the disability is temporary. Permanent Total Disabilities (PTD) can pay out to age 65 or pay a lump sum settlement. Permanent Partial Disabilities (PPD) will pay out less money than PPT's, but they may pay out for life or pay a lump sum settlement.

Workers' Comp Death Benefits

Death benefits can replace a portion of lost family income for dependents and eligible family members when an employee is killed on the job. Benefits may also be payable to parents when there are no surviving eligible dependent family members.

A beneficiary becomes eligible for death benefits the day after the employee's death. Death benefits end at different times depending on the beneficiary's qualifications to be entitled for this benefit. Death benefits may be paid if there is an eligible:

- Surviving spouse

- Dependent child

- Dependent grandchild

- Other eligible dependent family members such as parents may be eligible when there are no other surviving eligible dependent family members

Eligible Beneficiaries:

- A spouse is usually eligible to receive death benefits for life unless he/she remarries. Upon remarriage, the insurance carrier will typically pay a two (2) year (104 weeks) lump sum payment

- If there are minor children, the benefit is divided between the spouse and the minor children. One half is paid to the spouse and the other half is divided equally among the children

- Eligible children can usually receive death benefits until age eighteen (18) or twenty-five (25) if enrolled as a full time student in an accredited college. If there is more than one minor child, as a child loses eligibility the benefits are re-distributed among the other eligible children

Burial Benefits Covered by Workers Compensation

Burial benefits are paid to the person who paid the deceased employee's burial expenses. The maximum burial benefit allowed is usually between $4,000 and $12,500 depending on individual state law.

A beneficiary becomes eligible for death benefits the day after the employee's death.

Workers' Comp and Disability

Don't confuse disability insurance with workers' compensation disability payments. When you buy disability coverage you are buying an insurance product that pays a set amount of lost wages for injuries that happen off the clock. In other words, a disability insurance policy does not pay for injuries that would be compensable under workers' comp insurance. Conversely, workers' compensation insurance will not replace amy lost wages if an employees' injury was sustained outside of work.

It is not uncommon to see workers' comp claims where an injured worker claims they were injured at work even though the injury happened over a weekend. This type of fraud is frequently caught and employees can be fined and required to repay the insurance company.

There are three types of disabilities under workers' compensation insurance:

- Temporary Total Disability (TTD) Benefits

- Typically requires a waiting period of 3-7 days to be eligible

- Pays up to 66 2/3% of wages up to state weekly average (changes each year)

- Pays for a set amount of time which varies by state

- Permanent Total Disability (PTD) Benefits

- Pays up to 66 2/3% of wages up to state weekly average (changes each year)

- May pay up to age 65 in most states

- Permanent Partial Disability (PPD) Benefits

- Pays up to 66 2/3% of wages up to state weekly average (changes each year)

- May pay up to life in some states

Workers' Compensation Settlements

More than 70% of injured workers who receive disability end up with a workers' compensation settlement. The average settlement amount is ambiguous because its negotiated based on numerous factors including medical costs, lost wages, scarring, deformation, degree of impairment, future risks and more. Insurance companies often pursue settlements in order to receive future indemnification from the injured worked. In order to receive a settlement, an injured workers typically has to give up their rights to seek future damages from the insurance company and the employer.

The Business Owners' Role in Settlements

Settlement negotiations typically happen between the injured employee, their attorney and the insurance company. Employers should seek to be as helpful as possible, but business owners should remain neutral as the results are outside of their influence. While the cost of claims can affect an employers' experience modification rate, business owners need to let the insurance companies do their job and mitigate future liability for both parties.

Frequently Asked Questions- Workers' Comp Benefits

Can an employer cancel your health insurance while on workers' compensation?

No. An employer should not cancel and injured workers health insurance because they are two separate coverages. Employers are required by law to maintain the same level of health insurance benefits for a minimum of 12 weeks in most states.

Does workers' comp affect social security retirement benefits?

Yes it can. Retired employees may not be able to receive the full amount of both. SSDI will usually offset and be reduced based on a workers' comp settlement or benefit payments. An injured worker who becomes seriously disabled for more than 12 months, or permanently disabled, may be entitled to the payment of monthly Social Security benefits.

Can I choose my own doctor for workers' comp?

States are divided on this. Many states permit the employer and insurance company to direct medical and choose the treating physician. In some states like California, employees can provide written notice topredesignate who will treat then if the become injured. This can only be done if the employer provides a group health insurance plan. A few states do allow injured workers to direct their own care.

How much is a typical workers' comp settlement?

There is nothing typical about a workers' comp settlement because each case is unique. The average settlement ranges from a few thousand dollars up to $50,000 in the United States.

How long does it take to get workers comp settlement check?

A settlement often takes several months once an attorney is involved. Without an attorney settlement oftn happen as the medical portion of the claim is coming to an end. Once a settlement is reached, insurance companies typically pay the settlement in 30-60 days from signing the agreement.

How long does it take for workers' comp to kick-in?

Workers' comp coverage is immediate with regard to medical expenses related to an insurance claim. Payments for lost wages generally require a minimum of 3 days before lost wages will be replaced. Checks are usually send every two weeks so it may take up to 3 weeks to receive the first check.

How often do you get workers' comp checks?

Most insurance companies issue disability payments on a weekly basis. Most state laws indicate that injured workers should be paid at the sam frequency as they were paid normally. Insurance companies typically ignore this rules to reduce the administrative costs of weekly payments.

Can I go shopping while on workers' comp?

Injured workers are free to live their normal life while off work. Shopping is not very strenuous and does not prove an employee is capable of performing their normal work duties. It is legal for insurance companies to have investigators monitor some injured workers' when they suspect the potential for fraud. Soft-tissue injuries are especially hard to validate. There are countless examples where injured workers were filmed playing physical sports or lifting heavy object in their yard. Insurance can be a cat and mouse game sometimes- unfortunately.

How Does Workers' Compensation Work?

- What is Workers' Compensation?

- How Much is Workers Comp?

- Experience Modifiers & EMR Ratings

- Workers' Comp Class Codes

- 1099 vs W-2 Employee

- Workers Compensation Basics

- Employers Liability Insurance

- Workers' Compensation FAQ's

- Multi-State Insurance

- Workers' Compensation Laws

- State Insurance Fund

- Workers' Comp Claims

- Workers Compensation Benefits

- Managing Workers Comp Audits

- Workers' Comp Exemptions

- Ghost Policy

Save 30% on work comp for select businesses

Return to Work Programs Help

Save on Premium

Injured employees who remain off work longer than is medically necessary are more likely to:

- Develop complications that will lengthen their recovery

- Become depressed

- Focus on their pain and injury

- Lose physical conditioning

- Have higher claim costs

Employer should consider offering a Return to Work program when possible. Return to Work is set up by an employer to help injured employees go back to work quickly and safely while they heal. This can be done by either making changes to their regular job or placing them in a temporary or alternate work assignment that fits the restrictions as determined by their treating doctor. Employers should invest the time and effort in developing a Return to Work Program when possible.

Comp Quotes?

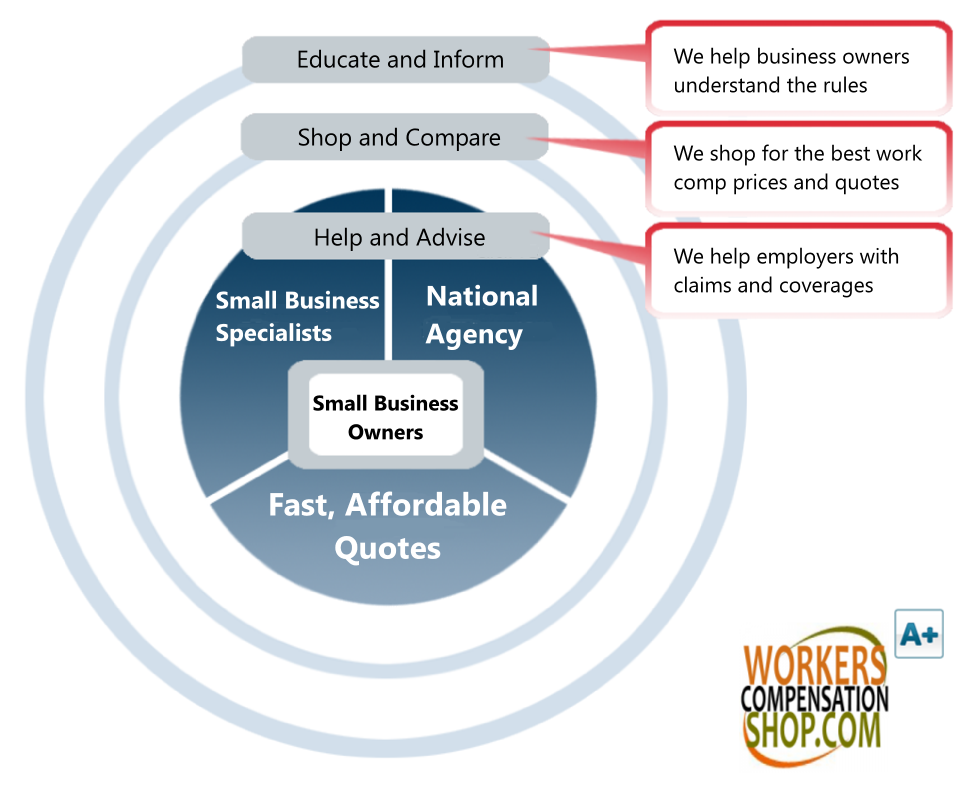

WHY SHOP WORKERS COMP WITH US?

We work with over 50 workers' comp insurance companies across the U.S. We compare rates and deliver your best deal.

We offer Pay As You Go Workers' comp plans and easy monthly payment options for your business.

We've developed Target Programs with our insurance companies to help find you the right insurance product with lower rates.

Workers' Compensation Laws by State

Workers' compensation benefits are set by each states. Our agency helps business owners manage their employers liability and workers' comp insurance.

Private insurance companies have different appetites and underwriting guidelines depending on their performance in each state. Workers' comp rates and pricing can vary tremendously from one carrier to the next. We're here to help you find the very best deal on coverage in your state.

If you have questions about your coverage or you think you might qualify for lower rates, contact one of our Specialist for a free no-obligation policy review. Talk to an expert at 1-888-611-7467 M-F, 8-5 CST.

California DBA: I-Shop Online Insurance Agency.