Experience Modification Rate- EMR Rating

A workers' compensation experience modifier automatically applies a pricing credit, or a debit, to adjust the rates and the price of a policy.

What is an EMR Rating?

Workers' Comp Experience Modification Rate- "Emod"

Workers compensation insurance experience rating is a mandatory program designed to measure and rate the risk of individual companies against other businesses in the same industry. Experience rating compares an employer's actual claims experience to the expected or average experience of all similar business types within a state.

An experience modification is developed and applied to risks with premium large enough for the insured's past experience to be an indicator of how much benefit, or claims, costs will be paid on behalf of the insured in the future. If an employer's past experience is better or worse than average, his premium is adjusted downward or upward by the application of the Emod, respectively.

In general, employer experience rating refers to a record of premiums and losses over the course of all applicable prior work comp polices. This provides a basis to predict future rates or costs for insurance carriers.

An employers' experience modification rate refers the factor calculated from actual loss experience amd used to adjust an the businesses manual premiums (higher or lower) based on the businesses loss experience relative to the average underlying manual premiums. The Modifier (X-mod) compares the insured experience to the average class experience.

Business owners and insurance agents use numerous interchangeable terms when referring to their experience modification rate. Synonyms include: EMT Rating, X-mod, Emod, ncci credit, mod rate, experience modification factor, ncci worksheet and EMR number.

What is the Purpose of Experience Rating?

The intent and purpose of experience rating is to incentivize business owners to take meaningful actions to reduce and prevent injuries. Workers comp manual rates group employers by their class codes, but that does not differentiate a business with no claims from a business averaging several claims a year. The business with no claims should pay less for coverage. The business with more claims should pay a larger share of the premium needed to provide for the cost of the claims.

How to Qualify for an Experience Modification Rate?

A business will not have an Emod for the first 1-3 years after it opens. Some very small businesses may never qualify for an experience modifier in some states. Qualifying for an EMR rating will vary by state, but the overall concept is the same. There are two triggers for qualification:

- Total policy premium exceeds dollar threshold for one policy period

- Total policy premium exceeds lower threshold for more than two policy periods

As an example, the state of Missouri has a one year threshold of $7,000 in premium before a business will be assigned and Emod and a Rating Effective Date (RED). Otherwise, the business will need premium to exceed $3,500 for more than two policy periods before it can qualify for an EMR rating. Each state sets their own dollar value for x-mod qualification.

Who Calculates Experience Ratings?

NCCI administers workers' compensation experience rating for 39 states. All business owners have a right to request their experience modification rate worksheet from NCCI or their state authority. States that administer their own EMR Rating programs include:

| California | Workers' Compensation Insurance Rating Bureau- WCIRB |

|---|---|

| Delaware | Delaware Compensation Rating Bureau- DCRB |

| Indiana | Indiana Compensation Rating Bureau- ICRB |

| Massachusetts | Workers' Compensation Rating and Inspection Bureau |

| Michigan | Compensation Advisory Organization of Michigan- CAOM |

| Minnesota | Minnesota Workers' Compensation Insurers Association- MWCIA |

| New Jersey | New Jersey Compensation Rating and Inspection Bureau- NJCRIB |

| New York | New York Compensation Insurance Rating Board- NYCIRB |

| North Carolina | North Carolina Rate Bureau- NCRB |

| North Dakota | Monopolistic |

| Ohio | Monopolistic |

| Pennsylvania | Pennsylvania Compensation Rating Bureau- PCRB |

| Texas | Texas Department of Insurance- TDI |

| Washington | Monopolistic |

| Wisconsin | Wisconsin Compensation Rating Bureau- WCRB |

| Wyoming | Monopolistic |

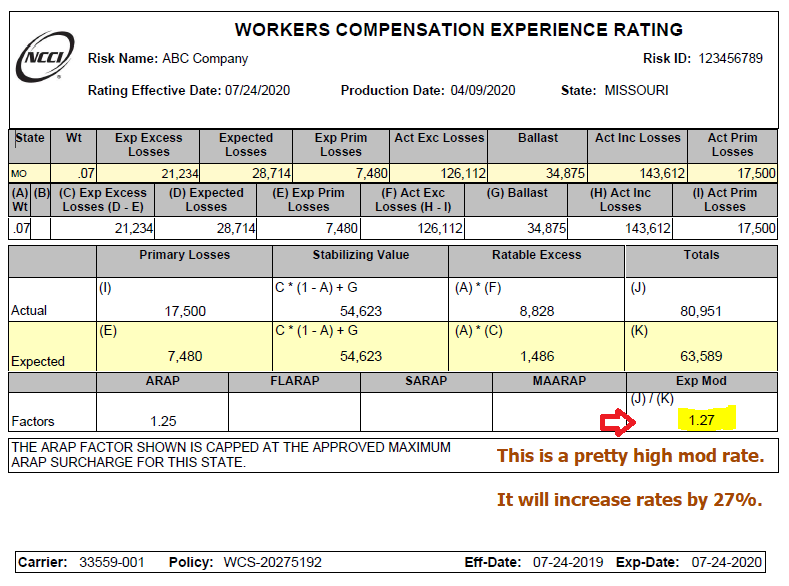

Here's Example of an NCCI Worksheet

The workers comp experience modification worksheet is a summary of claims and losses. It indicates how expected losses compare to actual losses over a period of time. Each year, qualifying businesses will receive a new Emod worksheet about 90 days prior to their Rating Effective Date.

Workers Comp Modification Factor

A modification factor is a factor applied to the policy premium for a risk to reflect variation from the experience of the average risk of a similar type. From the risk's own past experience, the experience modification rate is determined by comparing actual losses to expected losses. This comparison of future losses results in a premium reduction (credit) or a premium increase (debit).

For example, a modification of .85 results in a 15% credit or savings to the risk, while a modification of 1.10 produces a 10% debit or additional charge to the risk. In some cases, no change results and a modification of 1.00 (unity) is applied.

Experience Modification Factor (E-MOD)

In computing insurance premiums, experience modification factor refers to a provision for premium adjustment that recognized the merits or demerits of individual risks.

The modifier or "Emod" is a factor calculated from actual case loss experience, as reported on the unit statistical reports, used to adjust an insured's manual premiums (up or down). It compares the insured's experience to average class experience related to the same industries.

Workers' Compensation CLaims Costs- 3 Categories:

- Paid Losses:

Money spent on a claim

- Reserved Losses:

Money set aside (outstanding) for future payments

- Incurred Losses:

Combined total of paid plus reserved amounts

NCCI Credit Modifier

A credit experience rating modification lowers the net premium cost of the insured. A credit experience rating modification shows that the insured has less than average loss experience.

NCCI Debit Modifier

A debit experience rating modification increases the net premium cost of the insured. A debit experience rating modification shows that the insured has greater than average loss experience.

What is a Good EMR Rating?

The easy answer is that any experience modification factor below 1.00 is a good rating. Since 1.00 is average, or neutral, any Emod below 1.00 means that business is performing better than average for other businesses in the same industry and state. Some industries are expected to have more claims than others because of the associated risks. That is part of what drives rates and its why EMR Ratings are specific to industries.

What is the Lowest Experience Modification Rate Possible?

Each state will have specific elements that will affect the lowest possible Emod in that state. The lowest experience modification rate we've seen was an agency customer in California. Their mod rate was 0.48; so they were achieving significant savings on premium. This client had several million dollars in payroll and generated an annual premium over $250,000. They had no prior claims in an industry that normally has a frequent number of claims- hospitality.

As an agency, we've worked with client Emod's well over 2.00. Most commonly, we see a range of mod rates between .80 and 1.50.

What Affects your EMR Rating?

Think of an experience modification rate a a look back at your coverage history. Three years of policy information is used when calculating the EMR Ratings of each Rating Effective Date. The most recent past policy is excluded. Experience rating is only looking at the 3 years of coverage prior to the most current past policy. Therefore, a 2020 Emod would be based on policies that expired in 2018, 2017 and 2016.

Their are 3 important thing to consider when trying to understand how experience modification factors are influenced:

- Premium

- Overall cost of losses or claims

- Frequency of losses or claims

Premium is an important factor because it impacts the ratio between expected losses and actual losses sustained during a policy period. Expected losses are the average expectations for the cost of claims during the policy. Ultimately, the goal is to have actual losses come in under expected losses. This will generate a credit modification factor below 1.00. Frequency is also part of the equation because it increases the odds of having an expensive claim.

We leverage your EMR Rating to negotiate better deals with insurance companies.

Develops Over Time?

All new employers purchasing workers comp start out with a 1.00 modification factor. This means there is no plus or minus (credit/debit) modification adjustment on your insurance rates.

Over time, many employers will begin receiving an NCCI or state modification notice 60 - 90 days prior to their annual renewal date. Your insurance company will also receive the notice and will adjust your renewal prices accordingly.

An experience modifier rate under a 1.00 factor is a positive experience and means you will be rewarded for having little to no claims with a credit modifier. An Emod rate over a 1.00 factor means you are above the industry norm for claims in your state, based on your class codes.

X-Mod Example:

If you receive an experience modification rate notice that indicates your Emod is changing to 1.10, it means that your insurance carrier (or any other provider) will charge you an additional 10% for your workers comp rates. Conversely, a .90 modifier means you will pay 10% less on your next renewal policy.

Our Workmans Comp Specialists are trained to review and analyze experience modification rates and worksheets to help ensure that your mod rate is accurate and appropriate. We will work with you on strategies to help you reduce your experience modifier over time in order to correct prior debit Emod's.

Get a free insurance comparison today and see if your business qualifies for lower rates.

How Does Workers' Compensation Work?

- What is Workers' Compensation?

- How Much is Workers Comp?

- Experience Modifiers & EMR Ratings

- Workers' Comp Class Codes

- 1099 vs W-2 Employee

- Workers Compensation Basics

- Employers Liability Insurance

- Workers' Compensation FAQ's

- Multi-State Insurance

- Workers' Compensation Laws

- State Insurance Fund

- Workers' Comp Claims

- Workers Compensation Benefits

- Managing Workers Comp Audits

- Workers' Comp Exemptions

- Ghost Policy

A business owner has the ability to request copies of their experience rating worksheet from any state authority, or NCCI, depending on the state. Business owners can call NCCI at 800-622-4123. Choose option 4 once connected. Owners may be asked detailed company information, such as FEIN, to confirm ownership. NCCI will email the experience mod worksheet to the owner. This service is free to business owners.

Insurance agents and carriers can order a basic snapshot showing the current Emod for a business. This document is less detailed than the full NCCI Worksheet because it does not show the loss details for the past policies. Agents are required to obtain a signed Letter of Authority from the business owner in order to request the full worksheet from NCCI.

Save 30% on work comp for select businesses

An EMR Rating is a numerical factor used to manipulate a carriers filed workers comp rates. Here are a few ways to think of experience rating:

- The comparison of the basis of premium (usually payroll) and losses developed by an employer during a policy period or group of policy periods.

- The loss record of an insured.

- The history established by a risk as disclosed by the losses and the payroll appearing on the unit card. The premium paid is compared to losses paid out on an insurance policy.

- The aggregate premium or losses developed within a state during a period of time as reflected in a financial call.

How do I get started?

- Business details, locations, FEIN or SSN

- Estimated annual payroll and job duties- class codes

- Claims info or loss history- if applicable

- Experience Modification Rate- if applicable

Learn About Experience Rating and Rates in Your State

Ready to Start Your Quote?

Don't settle for cookie-cutter rates

- Secure

- Fast

- Easy

California DBA: I-Shop Online Insurance Agency.