Workers Comp Insurance Commission

Agents earn commission from insurance companies in exchange for writing and servicing a workers compensation policy.

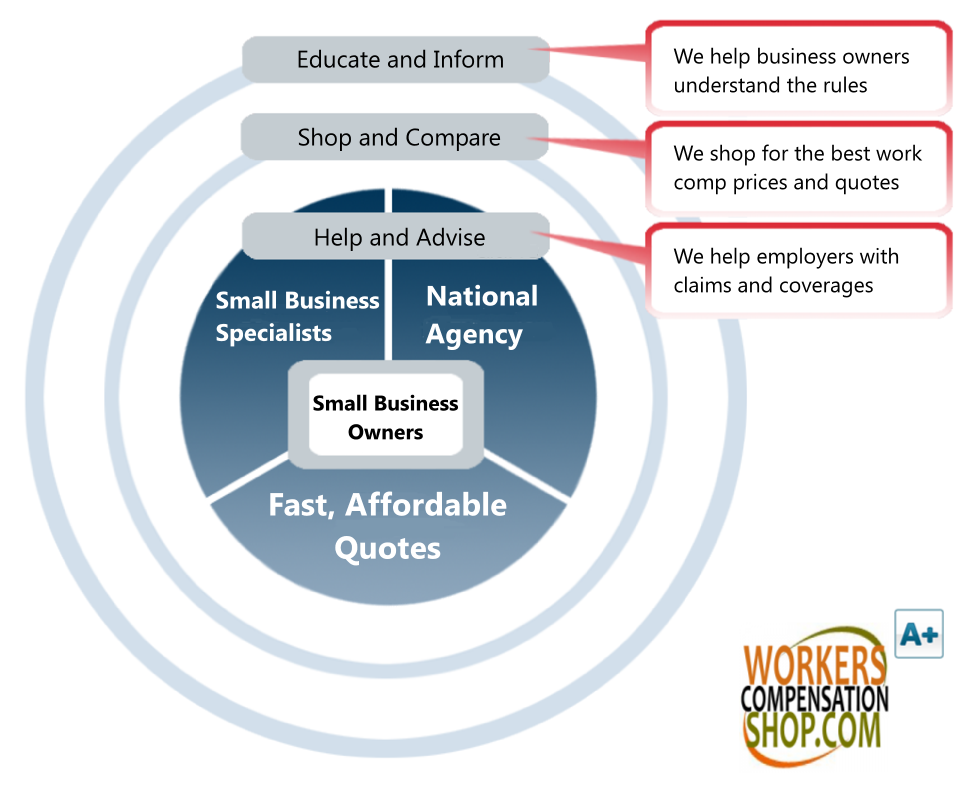

What Should I Expect From My Agent?

- Secure

- Fast

- Easy

How Insurance Agents Earn Commission

Insurance Commissions

Workers' compensation commission refers to the amount of premium paid to an insurance agent or agency by an insurance carrier for writing and servicing an insurance policy. While most agents and agencies prefer not to disclose commission information, we believe it is important to help our clients and prospects understand how the insurance and workers' compensation insurance commission system works.

Once an agent binds an insurance policy, the insurance company pays the agency a percentage of the total premium as a sales commission. Commission is either in full (estimated annual commission) or as earned (paid out as premium is received by the carrier. The agency may receive a chargeback on commission if the policy cancels early or the annual premium is lower than quoted premium.

The agency is responsible for paying individual agent commission for each producer working for the agency. The agency is also responsible for covering all other operating costs associated with marketing and servicing the policy including customer services staff, I.T., accounting, risk management, and account managers.

Work Comp Insurance Commission Defined

Insurance commission is fee paid to an licensed agent or agency for transacting a sale of an insurance policy or performing a service.

Commission is almost always paid as a percentage of gross premium. However, in some cases, carriers will also allow fee based commission as well as a reduced commission percentage on larger premium programs or more non-traditional products such as workers compensation retro plans, captives, and high deductible programs.

Workers comp insurance carriers actually pay varying amounts of workers' compensation commission. Commission percentage amounts can vary depending on the

- the state,

- an agencies total dollar amount of premium,

- the combined loss ratio of the written premium, or

- a combination of these factors. Many carriers may also reduce the commission payout as the premium size increases.

Most carriers will typically pay somewhere between 8% and 12% commission to an agent or agency. When agents work for an agency or with a middleman such as a wholesaler or broker they will most likely receive about 50% of the earned commission.

A Good Agent Should Earn Their Commission

Insurance agents and agencies should provide your business with valuable tools when shopping for coverage, including:

Consulting and advising clients prior to carrier submission underwriting

- Your agent should have a thorough knowledge of class codes, laws, and underwriting

- Your agent should be looking for areas to save you money

- Your agent should be willing and able to give direct advice on work comp rules and laws

Provide affordable quotes and options for your workers comp coverage

- Your agent should have multiple carriers and markets to provide you the best value and most options available

Issue certificates of insurance and provide ongoing service

- Your agent should issue all certificates or evidence of insurance timely and as needed

- Your agent should be available for consultation regarding policy changes

Assist with Claims and Renewals

- Your agent should be willing to guide you during the claims process

- Your agent should remarket your coverage each year prior to your renewal

Broker of Record Letters (BOR's)

Business owners are sometimes presented with Broker of Record letters and asked to sign them by another agent or payroll provider. A BOR is a document that changes the agent of record with the insurance company and assigns future commission and agency service rights to the agent requesting the document. Sometimes a business owner does not understand what the letter does, or they have a reason for not wanting to work with the existing agent or agency. Another common reason for a BOR is that a business owner simply prefers to consolidate their coverages with one agency.

Each insurance carrier establishes their own procedures for handling Broker of Record Letters. Most carriers generally choose to either a) recognize them immediately, b) recognize them at renewal, or c) reject the BOR altogether. Our agency policy is to allow Broker of Records bilaterally and assist our customers regardless of whether they are moving a policy to us or moving it to another agency.

Helpful Resources

Broker of Record Letter (sample)

State Fund Agency Commission

State fund coverage is generally considered the policy of last resort. State fund plans typically provide coverage to business owners who are not able to buy workers comp insurance from a private insurance company. Employers and agents generally turn to state fund options when an employer is in a high risk industry and their NCCI class codes are not codes private carriers want to cover, or they have had too many prior claims, or losses.

Most state fund programs only pay a nominal sales commission because they are not competing to write more coverage. On average, commission from or other state funds range from 3%-6% depending on the state and the size of the premium.

Workers Comp for Small Business Owners

Agents Should Earn Their

Commission

At Workers Compensation Shop.com, we're always ecstatic to win a new customer. We believe that personal and knowledgeable service goes a long way. And we want to keep your insurance business year after year.

That's why our Agents and Client Service Representatives undergo weekly product and industry training on workers compensation insurance. Our knowledgeable staff understands the various state regulations and rules for each workers' compensation policy. We specialize in Underwriting, Insurance Auditing, Pay As You Go Reporting, and Customer Service.

When you work with us, you get a team of professionals ready to assist you with quotes, policy changes, insurance certificates, renewals, and more. Best of all, you get a real person on the phone when you call- ready to assist you with coverage and questions.

PRICE CHECK

Get a free insurance comparison today and see if your business qualifies for lower rates.

How Does Workers' Compensation

Work?

- What is Workers Compensation?

- The Basics of Workers Comp

- Workers Compensation Q and A?

- Insurance Laws for Work Comp

- Managing Policy Claims

- Getting Work Comp Benefits

- NCCI Classification Codes

- Experience Modifiers and Ratings

- State Fund Insurance

- Workers Compensation Forms

- Handling Workers Comp Audits

- Understanding an Employer Liability Policy

- Excluding Owners and Officers

- Multi-State Coverage

Our Best Selling Workers' Comp Programs

Workers Comp Help?

- Can owners and officers exclude themselves from workers comp coverage?

- Understanding your workers compensation employers liability policy form?

- What is a workers compensation ghost policy?

- 10 questions you should ask your agent to save money?

- What insurance carriers do you work with?.

- I need a state workers compensation form?

- Workers Comp Questions and Answers?

WHY SHOP WORKERS COMP WITH US?

MORE THAN 35 CARRIERS TO QUOTE

We work with over 35 workers comp insurance companies across the U.S to shop your insurance coverage for the best price.

LOWER MONTHLY PAYMENT PLANS

With dozens of Pay As You Go and easy installment plans to choose from, you get more flexible options for your business.

EXCLUSIVE WORK COMP PROGRAMS

We've developed Target Programs with our insurance companies to help find you the right insurance product with lower rates.

California DBA: I-Shop Online Insurance Agency.